_11zon%20(1)%20(1)%20(1).webp)

Open Banking is a regulatory and technology-driven system that enables individuals to securely share their financial data with third-party providers such as fintech companies or other banks, with explicit consent. It allows people to make payments online with their bank accounts instead of using debit cards, manage multiple bank accounts in one place, access more personalised financial services, and receive tailored financial advice because service providers have a more holistic view of a user’s financial history. At its core, Open Banking is about giving bank consumers more control over their financial lives, encouraging innovation in financial services, and driving healthy competition in the banking sector.

Around the world, Open Banking is already transforming how people use their financial data. The model is driving the development of more efficient, inclusive, and responsive financial ecosystems by enabling tools such as budgeting apps and automated credit assessment systems. Nigeria is now building the infrastructure to join this global shift, marking a major evolution in how financial services will be delivered in the country.

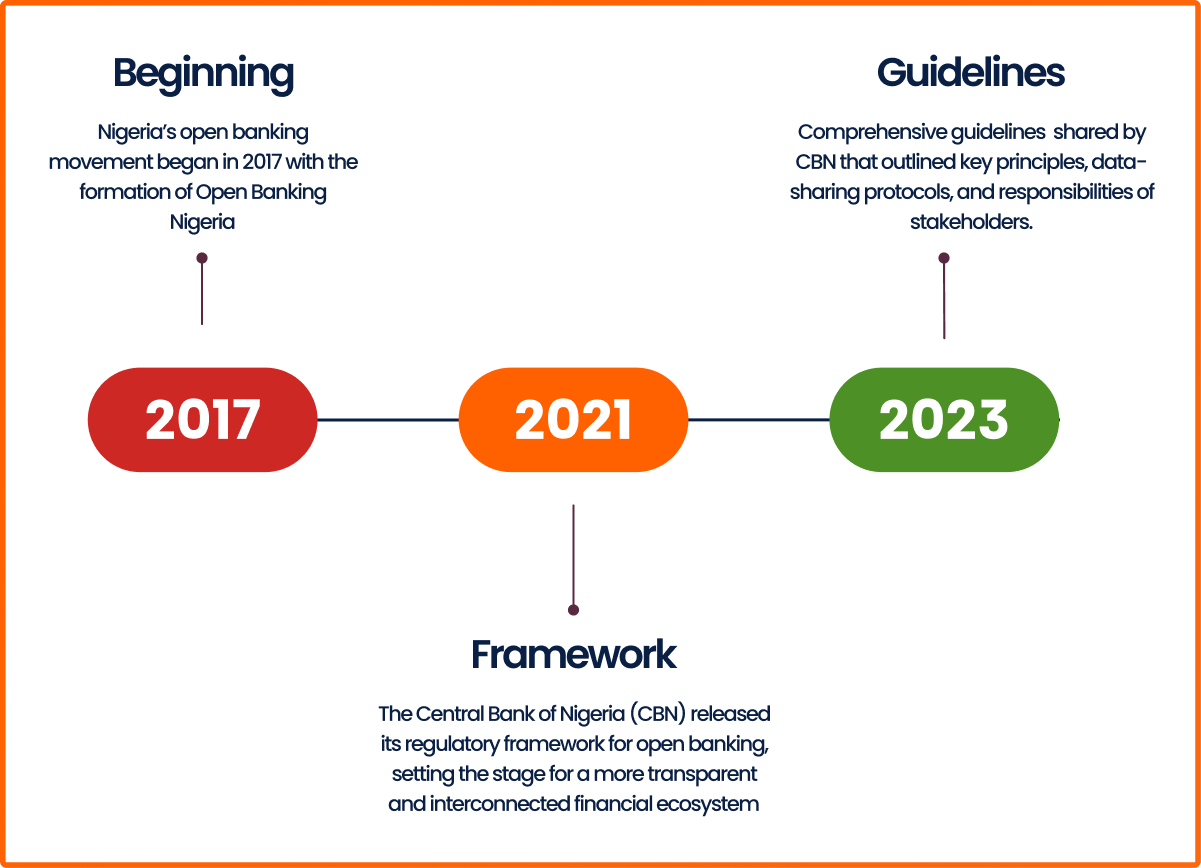

A Quick Look at Nigeria’s Open Banking Timeline

Nigeria’s Open Banking movement began in 2017 with the formation of Open Banking Nigeria, a group of technologists and financial experts working to develop standards and advocate for regulatory adoption. In 2021, the Central Bank of Nigeria (CBN) released its regulatory framework for open banking, setting the stage for a more transparent and interconnected financial ecosystem.

This framework was followed in March 2023 by comprehensive guidelines that outlined key principles, data-sharing protocols, and responsibilities of stakeholders. These included clear directives on how financial institutions must protect customer data, obtain consent, and enable interoperability through secure technology platforms.

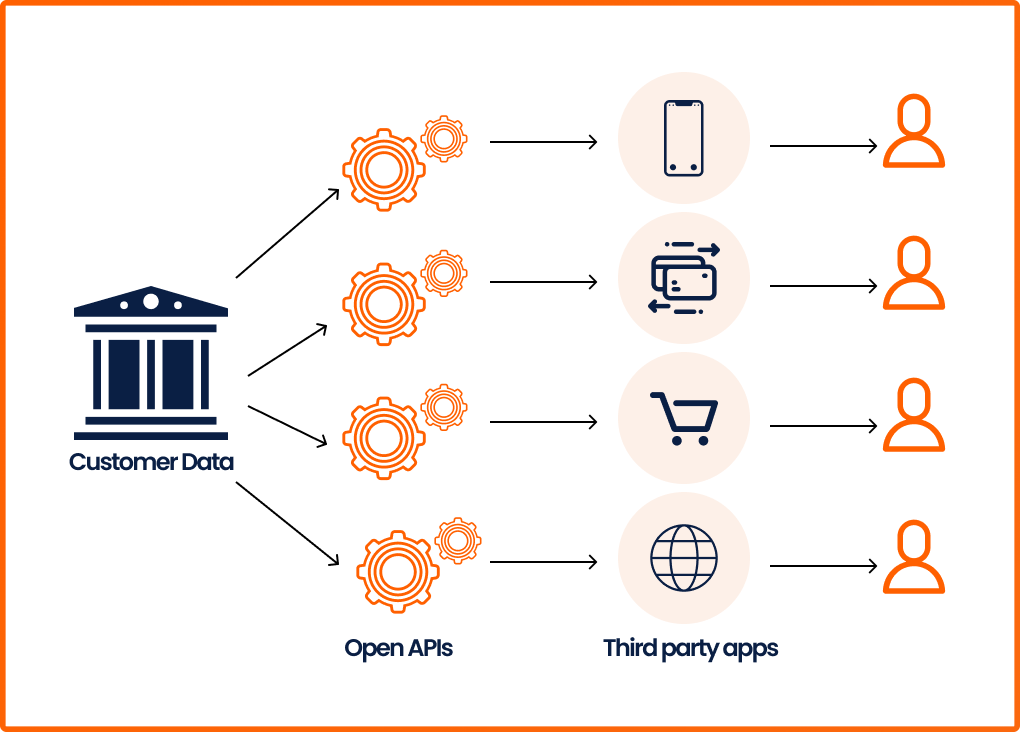

How Open Banking Works

Open Banking works through the use of Application Programming Interfaces (APIs), which is a way software and technology systems talk to each other. When a customer gives explicit consent, their bank can transmit specific financial information, such as transaction history or account balances, to an approved third-party provider. This could be an e-commerce site where customers want to make purchases, a budgeting app that helps track spending, a lender assessing creditworthiness, or another bank offering personalised services. APIs make this exchange fast, reliable, and secure, forming the technical foundation of the Open Banking system.

A key part of Open Banking is standardisation. Data sharing alone does not qualify as open banking unless it follows clear, shared formats that ensure information is exchanged in a structured, secure, and consistent manner. Just as important is the consent layer, which gives users full control over how their data is used. No information can be accessed without a customer's explicit permission. This combination of standardised processes and informed consent helps build trust in the system. Banks and Fintech regulated by the Central Bank of Nigeria are also required to follow strict rules, using secure platforms, protecting identities, and complying with data protection laws to ensure that Open Banking remains safe and reliable for everyone involved.

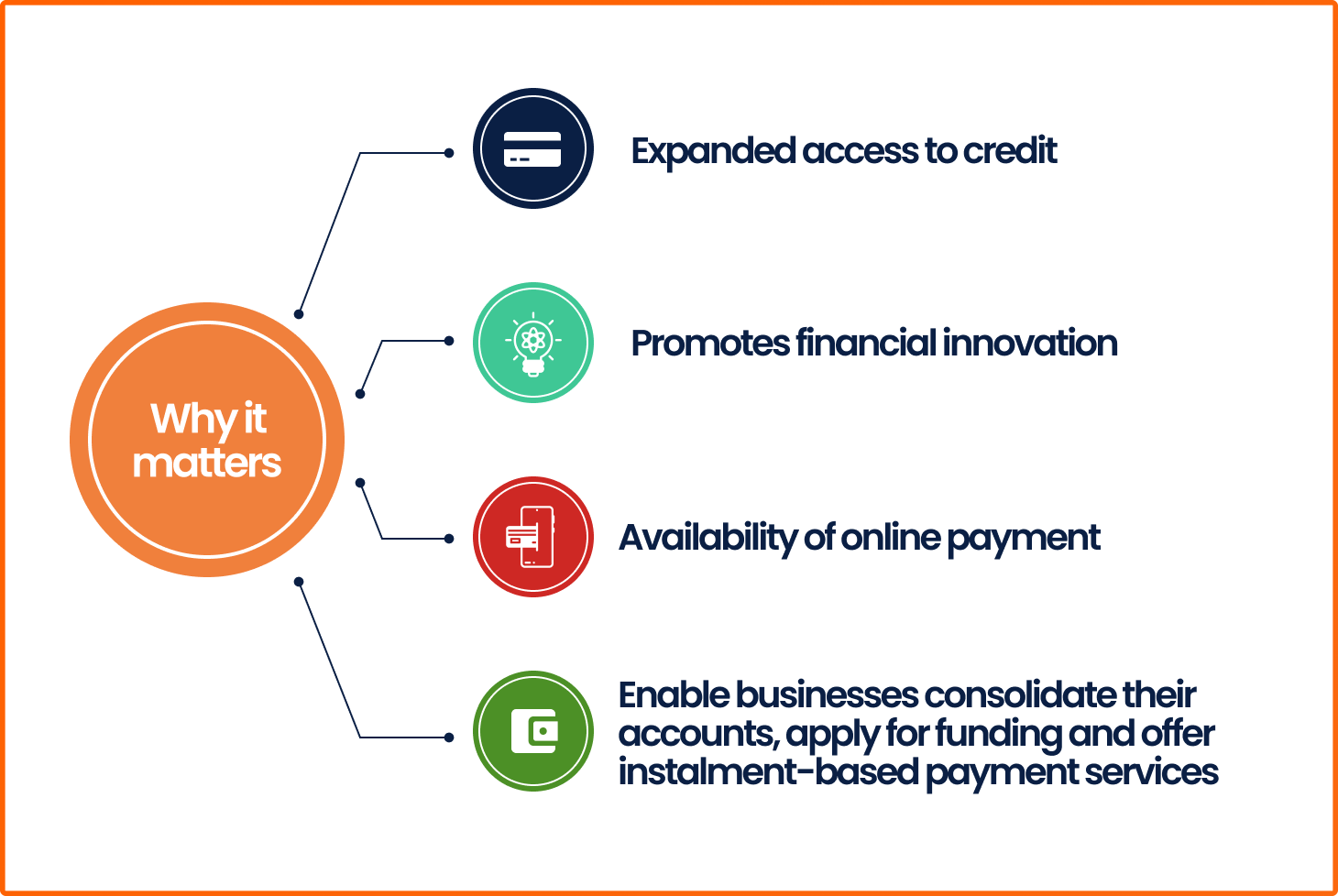

Why Open Banking Matters in Nigeria

Open Banking has the power to improve financial services in Nigeria in many ways. One of the most significant benefits is expanded access to credit. Many individuals, particularly those without formal employment or traditional credit histories, struggle to qualify for loans. With Open Banking, these individuals can share alternative financial data, such as mobile money transactions or e-commerce earnings, giving lenders a fuller picture of their financial activity and enabling more inclusive credit options.

The system also promotes financial innovation. By opening up access to financial data, Open Banking empowers fintechs and developers to build user-centric solutions. These include budgeting tools, loan comparison platforms, and other financial planning services designed to serve everyday people more effectively. This not only increases consumer choice but also encourages competition among providers, leading to better pricing and improved service delivery.

Perhaps the most immediate and far-reaching impact of Open Banking in Nigeria lies in online payments, where traditional card systems have consistently failed to deliver. In a continent where card penetration is low, card activation remains cumbersome, and successful transactions are rare, Open Banking presents a digital-first alternative. Customers can initiate secure direct bank transfers at checkout, eliminating the chaos of unreliable card systems, erratic OTP delivery, and failed settlements. This approach simplifies the payment experience for users and strengthens confidence among merchants who can receive funds more reliably. Real-time bank rails now support solutions that are redefining how Nigerians pay online, encouraging a future where seamless, cardless payments become the standard rather than the exception.

Moreover, Open Banking aligns closely with Nigeria’s ambition to grow its economy to one trillion dollars and beyond. To achieve this, the country must deepen financial inclusion, especially for young entrepreneurs and small business owners. Open Banking enables businesses to consolidate their accounts, track performance, apply for funding, and offer services like instalment-based payment systems. These tools improve operational efficiency and unlock new growth opportunities.

Who’s Involved: Key Stakeholders and Their Roles

Open Banking in Nigeria involves a broad coalition of stakeholders. At the centre is the Central Bank of Nigeria, which sets the regulatory tone and ensures financial institutions operate within approved guidelines. The Nigeria Data Protection Commission (NDPC) plays a complementary role by overseeing how customer data is handled and protected.

Banks are key custodians of financial data, while fintech companies bring innovation and agility. Their collaboration is critical for delivering real value to consumers. The Nigeria Inter-Bank Settlement System (NIBSS) is expected to provide technical support, ensuring interoperability and secure data exchange. Meanwhile, Open Banking Nigeria, the original advocacy group, continues to drive industry consensus and maintain implementation standards.

Challenges and Considerations

Open Banking introduces promising opportunities for financial inclusion and innovation, but it also brings important challenges that must be addressed. One of the major concerns is data privacy. Customers must be confident that their financial information is safe and used only with their explicit consent. Without strong safeguards and trust, many may hesitate to participate in Open Banking services.

Cybersecurity remains a critical consideration. As financial data flows across platforms and service providers, the risk of fraud, hacking, and misuse increases. Ensuring security requires coordinated action between financial institutions, fintech companies, and regulators. Clear frameworks must guide how data is accessed, stored, and protected. At the same time, public education is essential. Nigerians need to understand the benefits and risks of Open Banking and learn how to protect themselves from scams or unauthorised use of their data.

It is also important to clarify what Open Banking covers. In Nigeria, Open Banking is focused strictly on the banking sector, such as current accounts, savings, and loans under the regulation of the Central Bank of Nigeria. It does not apply to pensions, insurance, or capital markets. While these sectors may adopt similar data sharing models in the future, they are not currently part of the formal Open Banking ecosystem unless integrated through regulated fintech partnerships.

This distinction points to the broader concept of open finance, which expands beyond banking to include areas such as insurance, pensions, investments, and digital wallets. Open Finance remains a longer-term goal that would require multi-sector collaboration and regulatory alignment. For now, Nigeria’s efforts are concentrated on making open banking work effectively. Success in this area will lay the foundation for a more inclusive and comprehensive financial data system in the years to come.

Lessons from Other Countries

In the United Kingdom, Open Banking began in 2018 after a strong regulatory push by the Competition and Markets Authority. The nine largest banks were required to adopt common technical standards, allowing customer data to be shared safely and consistently. To support this, the Open Banking Implementation Entity was set up to oversee development and compliance. This structured approach focused on building trust and protecting consumers, while also creating space for innovation. Today, Open Banking in the UK enables millions of people to use services like budgeting tools, digital lending, and account aggregation, all of which help them manage their money more effectively.

Brazil equally adopted a broader and more integrated strategy by linking Open Banking with its wider financial reforms. It launched open finance in stages beginning in 2021, with the Central Bank of Brazil setting the pace through clear rules and timelines. A major feature of Brazil’s model is its integration with PIX, the country’s real-time payment system. This has made financial transactions faster and more accessible, enabling users to transfer money, apply for credit, and manage accounts across institutions using a single platform. The phased approach has allowed banks, fintechs, and regulators to adapt gradually, building stability and user confidence along the way.

India’s model focuses on building public infrastructure that supports digital financial services. Its Open Banking efforts are part of India Stack, a larger framework that includes the Aadhaar digital ID system, the Unified Payments Interface (UPI), and a consent-driven data-sharing mechanism known as Account Aggregators. Together, these tools give individuals control over their data and improve access to financial services, especially for underserved groups. This approach, backed by strong government commitment and a thriving digital culture, has allowed India to deliver financial innovation at scale. Nigeria can draw on these lessons while building its own model, especially given its strengths in mobile technology, its dynamic fintech sector, and the digital habits of its young population.

A New Era for Financial Services in Nigeria

Open Banking offers Nigeria a unique opportunity to reimagine its financial system. Making services more personalised, inclusive, and transparent can unlock access to credit, improve financial literacy, and empower entrepreneurs and small businesses. For Open Banking to succeed, collaboration is key. Regulators must offer clear and forward-looking guidance. Banks and fintech companies must prioritise consumer trust and innovation. The public must remain informed, empowered, and engaged in shaping this new financial future. With the right alignment of technology, regulation, and vision, Open Banking can serve as a foundational step toward a more dynamic, equitable, and resilient economy for all Nigerians.

%20-%20Edited.png)

.svg)

.png)

.png)

.png)

Ready to maximise open banking opportunities?

Assurdly helps businesses turn open banking visions into seamless and compliant solutions.

%20(1).jpg)

%20(1)%20(1).jpg)