%20(1).jpg)

When a financial institution receives its licence, excitement usually follows.

The product is ready. The team is ready. Customers are waiting.

Then comes the question.

“How long before we are live on Nigeria Inter-Bank Settlement System (NIBSS)?”

The answer depends on understanding the journey correctly.

Whether you are a Deposit Money Bank, Microfinance Bank, Mobile Money Operator, Payments Service Provider or another CBN-licensed entity, connecting to NIBSS follows a structured path. Some services are available broadly. Others, like NIP inward transfers, are restricted to deposit-taking institutions.

Here is what actually happens between licence approval and go-live.

Step 1: Licence Approval And Service Scope Clarity

Integration should begin only after regulatory clarity.

The institution must know:

- What services it is licensed to offer

- Whether it is authorised to take deposits

- Which NIBSS services it intends to activate

This matters because not all services are equal.

Most licensed institutions can integrate to services such as New Quick Response (NQR), Mandate Services and structured Debit Rails. However, NIP inward transfers, which allow an institution to receive interbank funds into customer deposit accounts, are restricted to deposit-taking entities.

Clarity at this stage prevents misalignment later.

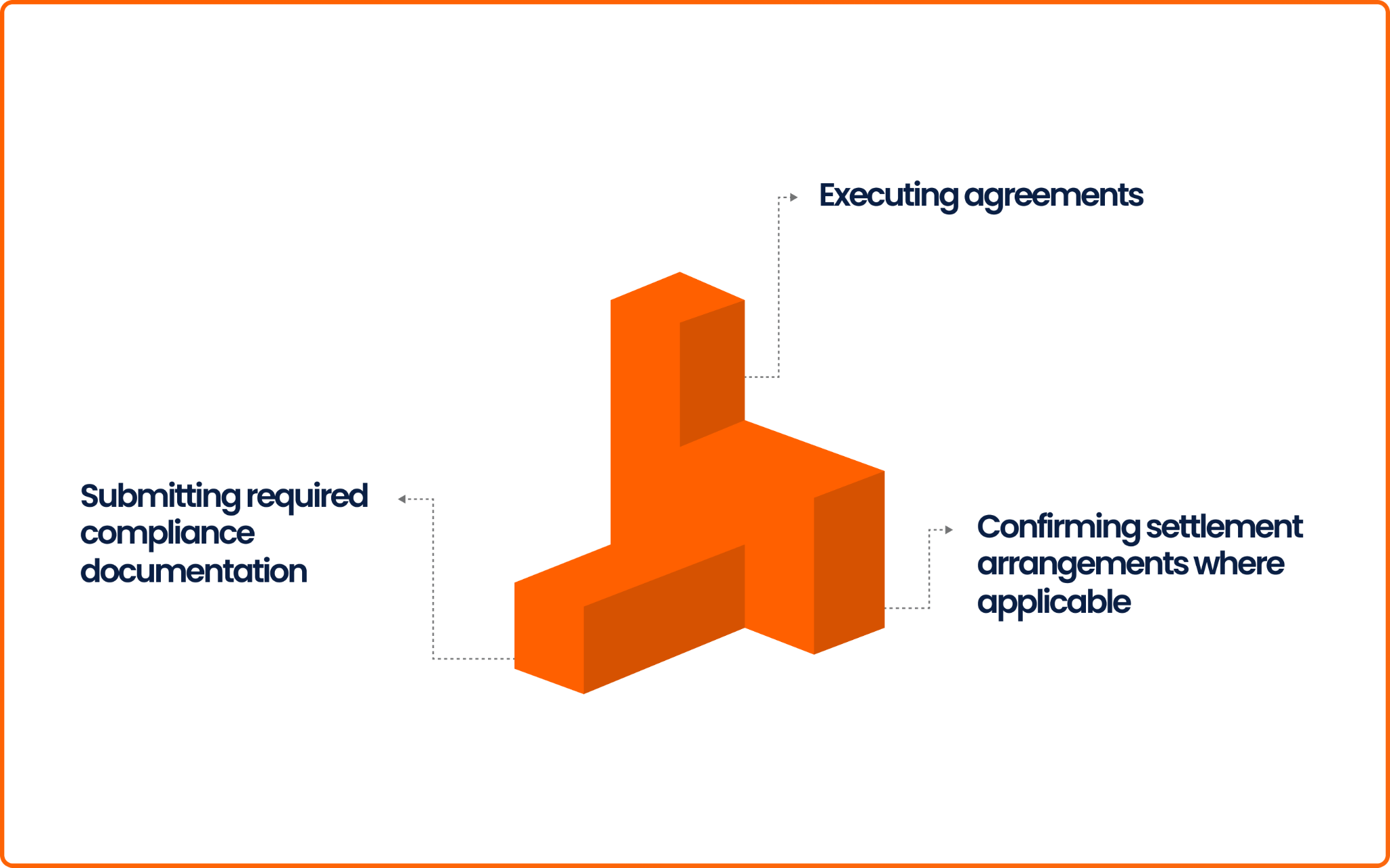

Step 2: Nigeria Inter-Bank Settlement System Onboarding

After licensing, the institution must formally onboard with NIBSS.

This involves:

- Submitting required compliance documentation

- Executing agreements

- Confirming settlement arrangements where applicable

Onboarding is not a technical formality. Production access is typically dependent on its completion.

Many timelines extend because onboarding is treated as secondary. It is not.

Step 3: Environment Access And Connectivity Setup

Once onboarding progresses, access to the NIBSS test environment is granted.

This includes:

- IP whitelisting

- Secure network configuration

- Endpoint validation

- Credential issuance

Without proper connectivity, integration cannot begin.

This stage requires coordination between internal infrastructure teams and NIBSS network teams.

Step 4: Core System Preparation (For NIP Inward Only)

If the institution intends to support NIP inward transfers, this step becomes critical.

NIP inward means receiving interbank transfers into customer accounts. For deposit-taking institutions, this requires the core banking or ledger system to correctly handle inbound credit flows.

NIP inward certification involves numerous predefined test scenarios. These cover successful credits, reversals, duplicate handling, timeouts and error responses.

During User Acceptance Testing (UAT), NIBSS personnel execute these test scenarios themselves.

If the institution’s system cannot respond correctly under these conditions, testing pauses. Lost testing windows can significantly delay go-live.

For institutions integrating only services such as NQR, mandate services or debit initiation, this level of core banking complexity does not apply in the same way.

Understanding whether NIP inward is in scope determines the depth of system preparation required.

Step 5: Integration And Internal Testing

The institution connects its systems to the selected NIBSS services.

This may include:

- NIP for outward transfers

- NIP inward for deposit-taking entities

- Mandate services

- NQR

- Other approved services

Internal testing is carried out before formal certification begins. This is where logic gaps should be resolved.

Step 6: Certification And User Acceptance Testing

Certification is where NIBSS validates behaviour.

For certain services, particularly NIP inward, NIBSS personnel run defined test scripts themselves.

If scenarios fail, corrections must be made before testing resumes. If testing stalls, institutions may lose their testing window and experience delays.

Clear communication and structured escalation during this stage shorten resolution cycles.

Certification continues until all required scenarios pass.

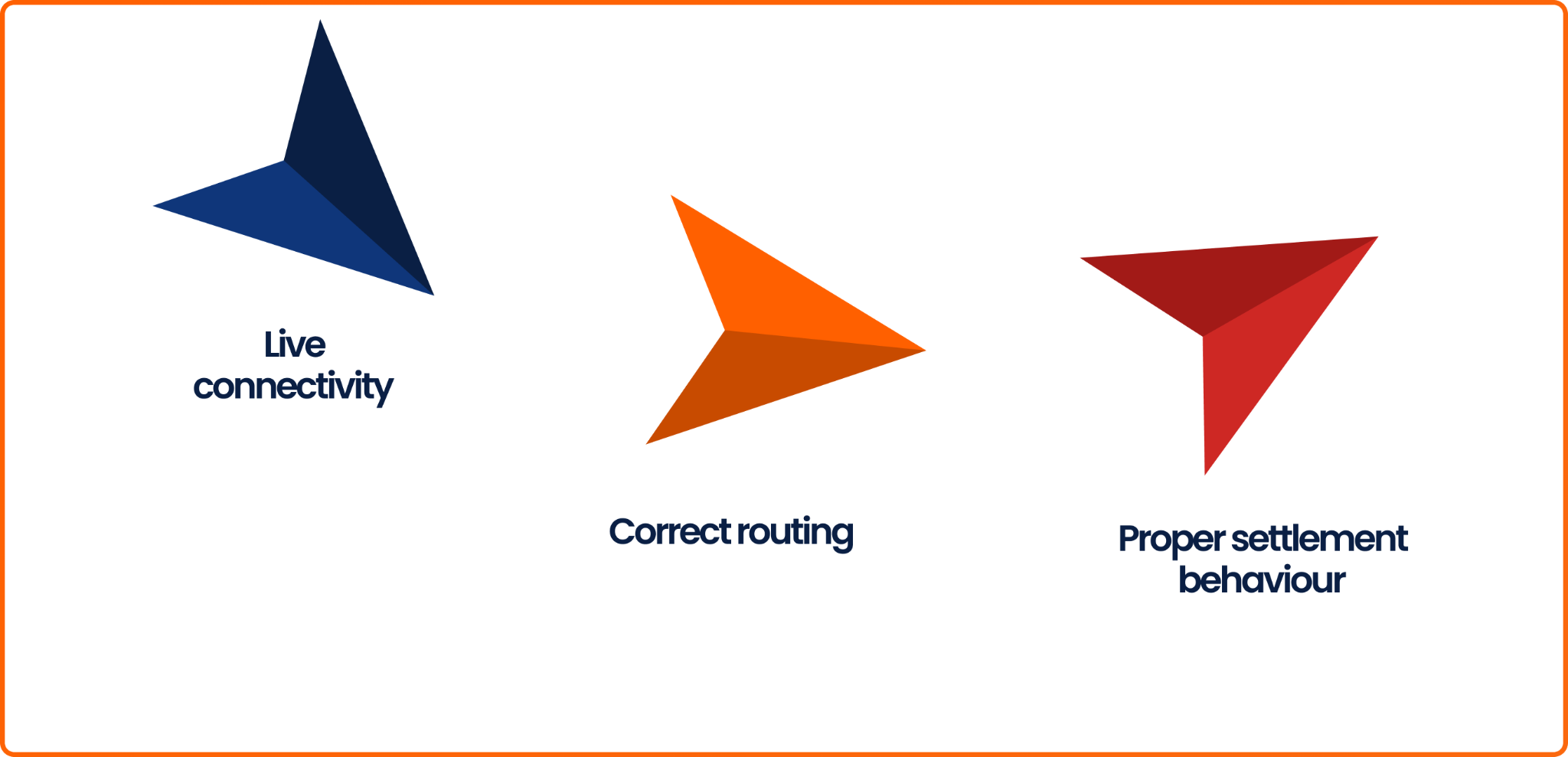

Step 7: Production Testing

After successful certification, the institution proceeds to production validation.

Production testing confirms:

- Live connectivity

- Correct routing

- Proper settlement behaviour

Limited live transactions may be executed under supervision to ensure everything behaves correctly in the production environment.

This step ensures that what worked in test works in reality.

Step 8: Go-Live

Once onboarding is fully completed and production validation succeeds, NIBSS activates the institution for live participation.

At this point, the institution can operate on its approved rails within the national payment ecosystem.

Go-live marks operational readiness. Monitoring and operational oversight continue from this point forward.

Why Timelines Differ

The journey itself is structured and predictable.

Delays occur when:

- Onboarding documentation is incomplete

- Settlement arrangements are not aligned early

- Core systems are unprepared for NIP inward testing

- Testing windows are lost

When these steps are approached deliberately and in sequence, the path from licence to go-live becomes manageable and clear.

Where A Structured Integration Framework Helps

At this point, the journey may look straightforward but heavy.

Each step is manageable on its own. The challenge is keeping them aligned. Onboarding must progress while connectivity is configured. Core systems must be ready before certification begins. Production validation must not expose gaps that could have been addressed earlier.

This is why we built NIBSS-in-a-Box.

It is not a shortcut around the process. It is a structured integration framework designed to move through the process correctly.

%20-%20Edited.png)

.svg)

.png)

.png)

.png)

Integrate with NIBSS today

Ready to integrate with NIBSS in record time? Contact our team today, and we will get you onboarded fast and easy.

%20(1).jpg)

%20(1).jpg)

%20(1)%20(1).jpg)